Gold vs Real Estate: Best Investment in Pakistan 2026

Deciding between Gold vs Real Estate is now the defining financial question for Pakistani investors in 2026. With inflation cooling to around 7%, the State Bank of Pakistan’s policy rate dropping from 22% to 10.5% in under two years, and geopolitical uncertainty reshaping global markets, the investment landscape has shifted dramatically from where it stood in 2025. Both gold investment in Pakistan and real estate investment in Pakistan delivered historic gains last year — but the dynamics heading into 2026 are completely different.

Whether you are a salaried professional looking to protect your savings, an overseas Pakistani sending remittances home, or a seasoned investor rebalancing your portfolio, understanding how these two asset classes perform in Pakistan’s current economic conditions is not optional. It is the difference between growing wealth and watching it erode.

Current Gold Price in Pakistan 2026

Gold prices in Pakistan have been on a historic bull run. According to live data from the All Pakistan Gems and Jewellers Sarafa Association (APGJSA) and tracked by Business Recorder:

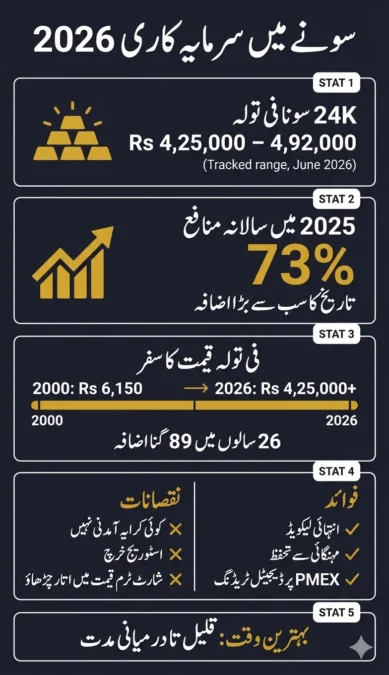

- 24K gold per tola: Rs 425,000 – Rs 492,000 (range tracked in June 2026)

- 24K gold per 10 grams: Rs 365,000 – Rs 422,000

- 22K gold per tola: Rs 390,000 – Rs 451,000

- International price: $4,100 – $4,700 per ounce

These gold rates in Pakistan are updated daily by the Karachi Sarafa Market and remain broadly consistent across Lahore, Karachi, Islamabad, Rawalpindi, Peshawar, and Multan, with minor city-to-city variation.

The more important number is the year-on-year return: gold in Pakistan delivered an astonishing 73% return in 2025, rising from approximately Rs 233,000 per 10 grams at the start of 2025 to over Rs 405,000 by December — the first time in Pakistan’s history that 10 grams of gold crossed the Rs 4 lakh mark. In 2026, prices have continued to surge before a partial correction began in late May and June as international prices pulled back from their $4,700 peak. The 1-year return as of June 2026 still stands at approximately +22%, even after the recent dip.

Over a 26-year horizon, gold has moved from Rs 6,150 per tola in 2000 to Rs 425,000+ today — an 89x increase — making it one of the strongest long-term stores of value in Pakistan’s financial history.

Gold Investment in Pakistan 2026: Full Picture

Why Pakistanis Trust Gold

Gold’s role in Pakistan goes far beyond investment. It is a cultural asset, a wedding necessity, a savings instrument, and an inflation hedge — all in one. When the Pakistani rupee lost over 81% of its value against the US dollar between 2000 and 2025, gold holders were protected. PKR-denominated gold returns massively outperformed rupee depreciation because gold is globally priced in USD, meaning every devaluation of the rupee directly amplifies gold’s PKR value.

This is precisely why gold remains the most trusted asset for households across all income levels, from jewelry buyers in Anarkali to institutional traders on the Pakistan Mercantile Exchange (PMEX), where investors can buy and sell gold futures contracts without physically holding the metal.

Pros of Gold Investment in Pakistan

High liquidity and instant access to cash. Gold is the most liquid hard asset available to Pakistani investors. A tola of gold can be converted into cash within hours at any Sarafa market, jeweller, or PMEX platform — no waiting for buyers, no documentation queues, no registration delays.

Proven inflation hedge. Every major inflation cycle in Pakistan — 2008, 2018–2019, 2022–2023 — saw gold prices surge. When inflation ran above 30% in 2023, gold protected purchasing power while savings accounts and fixed deposits offered negative real returns.

Portfolio diversification anchor. Gold’s low correlation with equities means it holds or gains value when the stock market corrects. In early 2026, when the KSE-100 corrected approximately 10.5% year-to-date, gold continued to serve as a stabilising force in diversified portfolios.

Zero management burden. No tenants, no maintenance, no legal disputes, no utility bills. Gold sits in a locker and preserves value passively.

Low entry point. You can start investing in gold with as little as one gram, making it accessible to middle-income and salaried Pakistanis who cannot afford a property down payment.

PMEX access for digital gold investing. Investors who want gold exposure without physical storage risks can trade gold futures on PMEX. This is particularly useful for younger, tech-savvy investors who prefer screen-based trading.

Cons of Gold Investment in Pakistan

No passive income. Gold generates zero cash flow. It sits in a vault and either appreciates or depreciates — there is no monthly rental cheque, no dividend, no yield. For investors who need income from their capital, gold alone is insufficient.

Price volatility in the short term. As witnessed in June 2026, gold can drop Rs 9,000–12,000 per tola in a single session when international markets correct. Short-term traders face meaningful price risk.

Storage and security cost. Physical gold requires a bank locker (Rs 3,000–8,000 annually) or a home safe, both of which carry theft and insurance considerations. These costs quietly erode net returns.

Making charges on jewellery. If you invest through gold jewellery rather than bullion or coins, making charges of 5–25% significantly reduce effective returns when reselling.

Currency risk on the upside. Gold’s extraordinary 2025 returns were partly driven by rupee weakness. If the PKR stabilises or appreciates, gold’s PKR returns will compress even if international prices hold steady.

Real Estate Investment in Pakistan 2026: Full Picture

Pakistan’s property market in 2026 is operating in conditions that rarely align simultaneously: inflation at generational lows, falling interest rates, regulatory reform, rising remittances, and a regional ceasefire that has restored investor confidence.

Pakistan Property Market 2026: Key Numbers

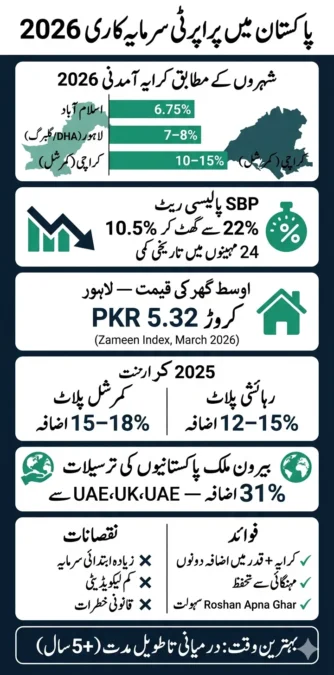

- Average house price in Pakistan: PKR 5.32 crore (Lahore, per Zameen March 2026 price index)

- Residential plot appreciation 2025: 12–15% annually

- Commercial plot appreciation 2025: 15–18% annually

- Rental yield in Islamabad: ~6.75% gross annual

- Rental yield in Lahore apartments (Gulberg/DHA): 7–8% net

- Rental yield in Karachi: ~6.21% average, with commercial properties reaching 10–15%

- Sector CAGR projection 2025–2029: 4% (real estate portals)

- Remittance surge: Over 31% increase in recent period, injecting massive liquidity into property markets

The State Bank of Pakistan’s policy rate reduction from 22% to 10.5% is the single most transformative macro factor for real estate in 2026. Lower rates mean cheaper mortgages, more developers entering the market, and more buyers able to finance purchases — all of which push property values upward.

Growth Drivers in Pakistan’s Real Estate 2026

Falling interest rates and mortgage access. With the SBP rate at 10.5%, Roshan Apna Ghar mortgage products have become meaningfully affordable, particularly for overseas Pakistanis investing remotely. Buyers who sat on the sidelines through 2024 are now actively entering the market.

Remittances and overseas Pakistani demand. Remittances rose over 31% recently, with overseas Pakistanis from the UAE, Saudi Arabia, UK, USA, Canada, and Australia channelling capital into DHA projects, Bahria Town, gated communities, and emerging societies across Lahore, Islamabad, Karachi, and Gujranwala.

Infrastructure-led appreciation corridors. The Rawalpindi Ring Road is reshaping the twin cities’ property geography. The M9 Motorway is driving suburban Karachi growth. DHA Gujranwala’s post-ballot development has created a new investment hotspot. Wherever infrastructure moves, property values follow — and Pakistan is spending heavily on infrastructure in 2026.

RERA and regulatory reform. Pakistan’s government announced plans to establish a Real Estate Regulatory Authority (RERA) to bring transparency and buyer protection to an historically unregulated sector. Punjab is simultaneously developing a digital real estate regulatory system under the RERA Act framework. While implementation is still in progress, the direction of policy is firmly toward formalisation — which historically increases investor confidence and raises property values in organised markets.

Budget 2025–26 incentives. The federal budget introduced reduction in withholding tax, elimination of Federal Excise Duty on commercial plots, and new investor protection measures — all directly lowering the cost of property transactions.

Urbanisation and housing deficit. Pakistan’s population is growing rapidly, and urban migration into Lahore, Karachi, and Islamabad continues. The housing shortage means demand structurally outpaces supply in major cities, creating a durable floor under prices.

Pros of Real Estate Investment in Pakistan

Dual return engine: rental income plus capital appreciation. Property earns you both simultaneously. A well-located apartment in Lahore’s DHA can appreciate 10–12% annually while generating 7–8% net rental yield — a combined return that no savings account, bond, or gold holding can match on a risk-adjusted basis over a 5–10 year horizon.

Tangible, utility-bearing asset. Unlike gold, property has functional utility. You can live in it, rent it, develop it, or use it as collateral for financing. It is an asset that generates real economic activity.

Inflation protection with income. Real estate in Pakistan rises with inflation because both rents and property prices track the general price level over time. This means your asset is appreciating and your income stream is growing simultaneously — a powerful combination for long-term wealth protection.

Overseas Pakistani-friendly investment channels. Roshan Apna Ghar and Roshan Digital Account platforms make it easier than ever for non-resident Pakistanis to buy property remotely, with government-backed financing and online verification.

Leverage potential. Real estate can be purchased with partial financing, allowing investors to control a larger asset base with less capital. No other mainstream investment in Pakistan offers comparable leverage at current mortgage rates.

Cons of Real Estate Investment in Pakistan

High entry cost. Quality property in Lahore, Islamabad, or Karachi starts from several million rupees. For investors with limited capital, this is a meaningful barrier that gold does not impose.

Low liquidity. Selling property can take weeks to months depending on market conditions, buyer availability, legal due diligence, and documentation. In a liquidity crisis, a property owner cannot exit quickly the way a gold holder can.

Legal and documentation risk. Fake documents, disputed titles, NOC issues, and unauthorised societies remain real risks in Pakistan’s property market. Due diligence is non-negotiable. Always verify NOC status with LDA, RDA, CDA, or the relevant authority before purchasing.

Management responsibilities. Rental properties require active oversight — tenant management, maintenance, utility coordination, and dealing with vacancy periods. This is not a passive investment in the way gold is.

Location dependency. A property in the wrong location — far from infrastructure, in an unapproved society, or in a market with oversupply — can underperform or depreciate. Real estate returns are highly location-specific.

Gold vs Real Estate Pakistan 2026: Head-to-Head Comparison

| Aspect | Gold | Real Estate |

|---|---|---|

| Liquidity | Very High | Low |

| Passive Income | None | 6–15% rental yield |

| 2025 Return | ~73% (historic year) | 12–18% (residential/commercial) |

| 2026 YTD Return | ~+22% (with correction) | Steady appreciation |

| Entry Cost | As low as 1 gram | Millions of PKR |

| Inflation Hedge | Very Strong | Strong |

| Management Effort | Minimal | High |

| Risk Type | Global market, USD rate | Location, legal, local economy |

| Leverage Option | No | Yes (mortgage) |

| Tax/Documentation | Minimal | Requires legal process |

| Best Time Horizon | Short to medium term | Medium to long term (5–10 years) |

Which Is the Best Investment in Pakistan 2026?

Here is the honest answer: the best investment depends entirely on your capital size, time horizon, and income needs. There is no universal winner — but there is a clearly rational framework for each type of investor.

Gold is the better choice in 2026 if:

- You have limited starting capital (under Rs 5–10 lakh)

- You need to stay liquid and may require access to cash within 1–3 years

- You are primarily protecting savings against rupee depreciation

- You want zero management effort and no legal complexity

- You are adding a short-to-medium term hedge during global uncertainty

Real Estate is the better choice in 2026 if:

- You have sufficient capital for a meaningful entry (ideally 30–50 lakh or more)

- Your investment horizon is 5 years or longer

- You want passive income that grows with inflation

- You are an overseas Pakistani with access to Roshan Apna Ghar financing

- You want to take advantage of the current low interest rate window before rates rise again

Both assets together is the smartest approach in 2026. As noted by financial analysts in The Express Tribune, asset selection — not market timing — will define investor outcomes in 2026. Gold provides the liquidity buffer and currency hedge, while real estate delivers compounding income and capital depth. A portfolio with 30–40% in gold and 60–70% in quality real estate covers both short-term emergencies and long-term wealth creation.

The window for real estate entry is particularly compelling right now. Pakistan’s policy rate has fallen from 22% to 10.5% in under 24 months. This kind of rate environment is rare and historically short-lived. Investors who enter quality markets — DHA Lahore, Bahria Town, CDA-approved Islamabad projects, Karachi DHA — in 2026 are likely locking in both yield and capital appreciation simultaneously.

For gold, the 2025 bull run has created a high base. While gold remains a core holding for any Pakistani investor, chasing it at Rs 450,000+ per tola carries meaningful short-term risk. Systematic accumulation — buying a fixed amount monthly regardless of price — is the more prudent approach than lump-sum entry at current levels.